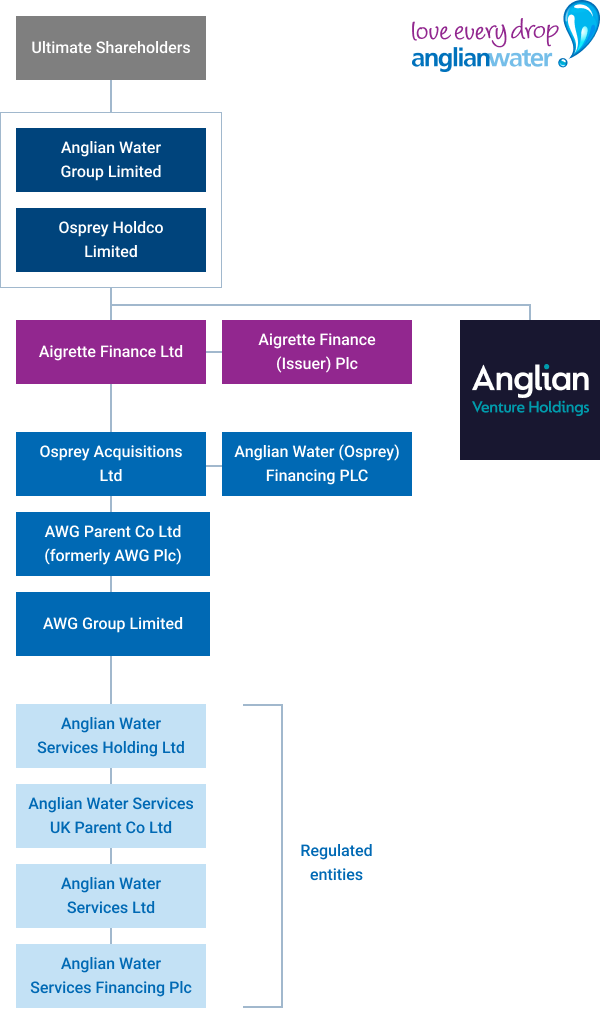

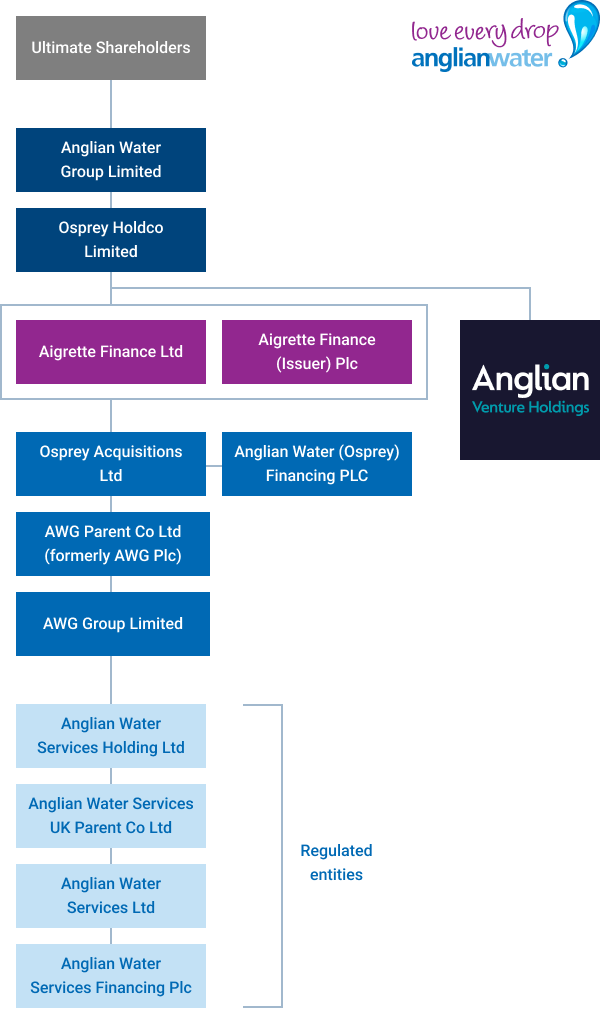

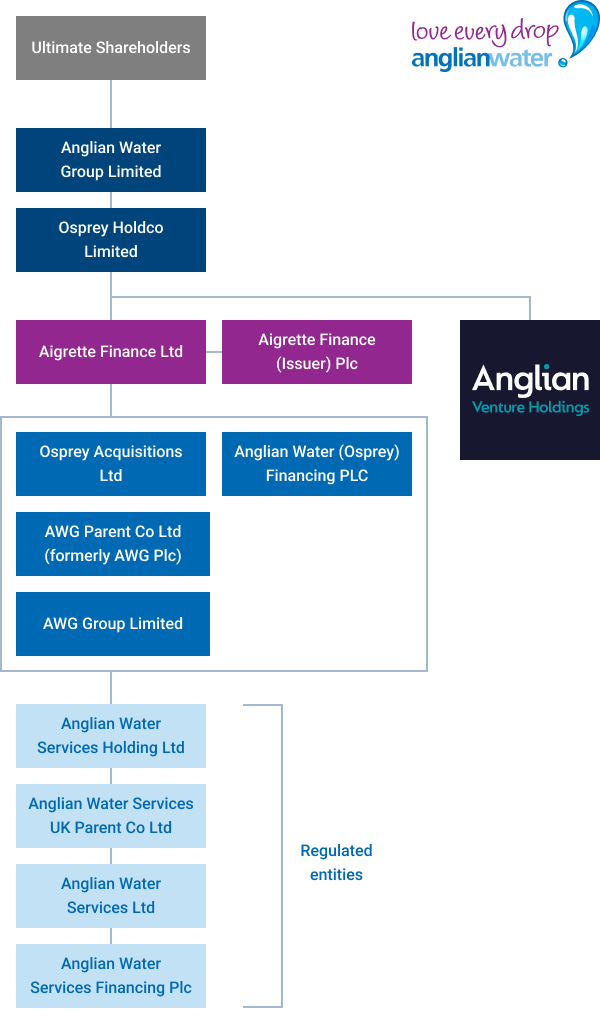

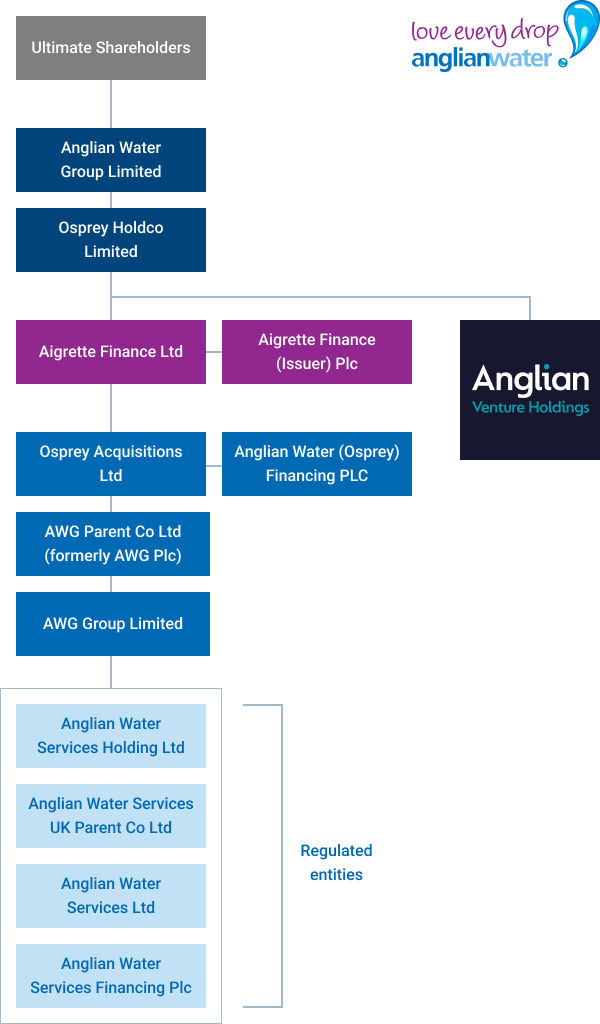

Group structure

The Anglian Water Group (AWG) has a comprehensive corporate structure designed to facilitate effective management and financing. Below you'll find an overview based on the 2025 Annual Integrated Report.

Group structure

Anglian Water Group operates with a three-tier financing structure, designed to efficiently raise and manage debt while maintaining strong credit fundamentals and regulatory ringfencing.